Applovin a profitable adtech champion

Amid the growth selloff some stocks are profitable.

Amid the massive sell off in ARKK-like stocks and the 2001 vibes, I decided to put something in written form for Applovin for the next reasons:

It is profitable. ( >20% EBITDA margins, and that doesn’t include SBC)

It grows, a lot. (The valuable segment is growing 100%, >50% organically)

Valuation is in the realm of sanity (25 times NTM EV/EBITDA)

I wasn’t sure how to start this write-up, I think that’s because trying to paint a picture of this company is extremely difficult due to the rapidly changing nature of the industry and the company. I honestly believe management has a clearer view of how the industry will look in 5 years than what role Applovin will be playing in that industry.

Applovin went from Adnetwork/ DSP to publisher of casual and hypercasual games (I strongly recommend you to read this article about Matchington Mansion's success and AppLovin connection with a shadowy Chinese studio publishing under an interposed brand, Firecraft, owned by Applovin. So you see how ruthless and secretive Applovin can be).

Then they acquired Adjust just ahead of the IPO, a German marketing measurement company. IMO Adjust needed first party data to keep their business viable after IDFA depreciation and Applovin needed Adjust to challenge FB and GOOG attribution tools and further integrate the advertisement ecosystem.

In October of 2021 they bought MoPub from Twitter. This move has synergies with their other businesses and gets Applovin into the supply side of the ad market, and although it is not the greatest business ever, there is a lot of information they now have access to.

Mobile advertising is a complicated industry, if you are not familiar with it you will hardly get a glimpse of what Applovin does. I am not an expert either - just a generalist - and what makes me be bullish on the company is a combination of past success and superb execution, the ambitious management team and what I think is great strategic positioning.

However, everything is so fluid with this company and this industry (IDFA has turned upside down what works in mobile advertising, for example) that I will just try to snapshot my evolving view on the company, without marrying too much with any projection or thesis.

The bull thesis

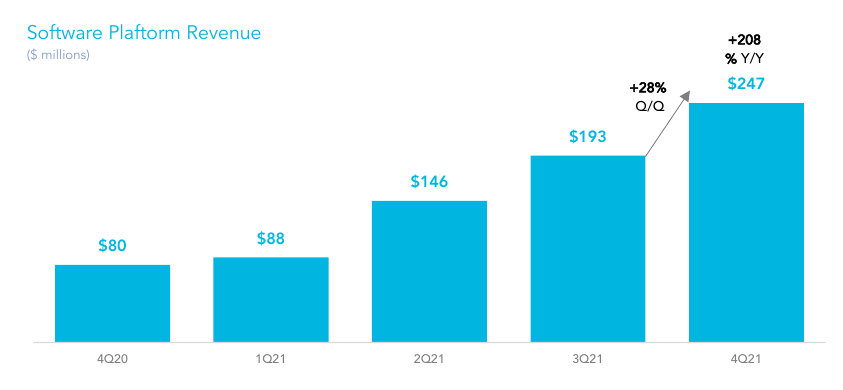

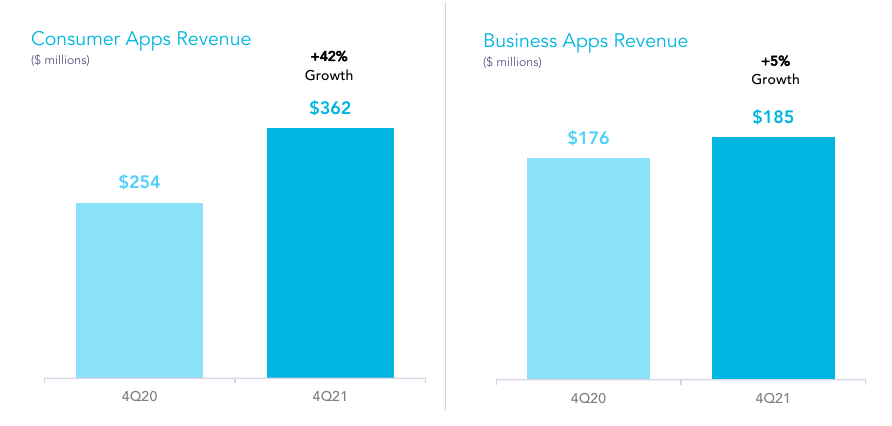

Applovin has two segments, what they call Software Platform Revenue which is all the adtech revenue they get from MAX, Adjust, MoPub clients and now Wurl outside of their own apps; and what they call Apps, revenue from either selling ad inventory in their games (Business Apps) or in-app purchases (Consumer revenue).

Although not entirely organic, Software Platform Revenue is growing nicely.

Consumer Apps revenue growth is more muted (can you spot how IDFA depreciation helps the adtech and hurts selling inventory?) and should command a lower multiple.

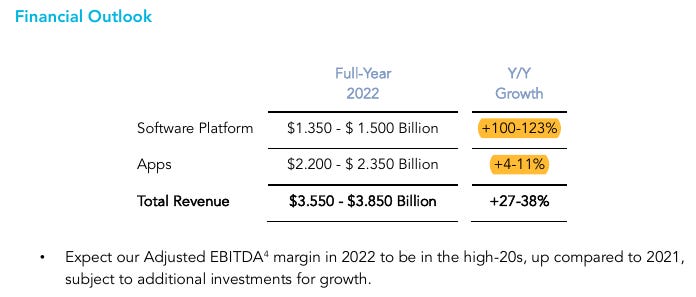

Although the company is deemed a huge player in the mobile gaming market, after a weak 2022 guide for this segment, management signaled that their core focus is the adtech segment, while Apps is merely instrumental to feed data to their Software Platform.

Here you can see management downplaying the Apps segment

If you read the Q2 2022 Conference Call you wouldn’t think Apps is a secondary segment to them:

Anyhow, I can tell you that the Software Platform Revenue should command a higher multiple. It is simple a better business with a wider moat than games, higher operating margins and better unit economics. They are widening their offering and although not in a position to challenge the TTD in CTV, they are the leaders in mobile gaming advertising and plan to use that stronghold to move into other markets.

They are clearly benefiting from Facebook losing their advantage in iOS, since the Apple depreciation of IDFA, Facebook doesn’t know who the user of the game is and thus cannot serve him the best ad - previously, FB had a “virtual file” on every user, so with their IDFA, they could track who that user was and whether they liked gardening from the likes on Instagram or he loved electronics from their comments on the blue app.

Also, once the ad has been served, it is complicated to track who downloaded which App, which messes up attribution and CPI (Cost per install). Several other players have had issues adapting to the new situation. Although I believe they will adapt and find ways of softening the blow, the playing field has been leveled.

Applovin and Ironsource, rely on first party data from their games and in fingerprinting to target and identify users. This has bolstered the offering of these companies (Although only Applovin has been clearly showing increased market share).

The bull case rests in Applovin being able to use their first party data as well as their seemingly superior mediation technology to keep wining share in mobile gaming and entering new app markets like health & fitness.

Applovin’s guide for 2022 revenue in the Software Platform segment implies around 60% organic revenue (assuming MoPub was doing $250M). Which is quite attractive for the margins the company already achieves.

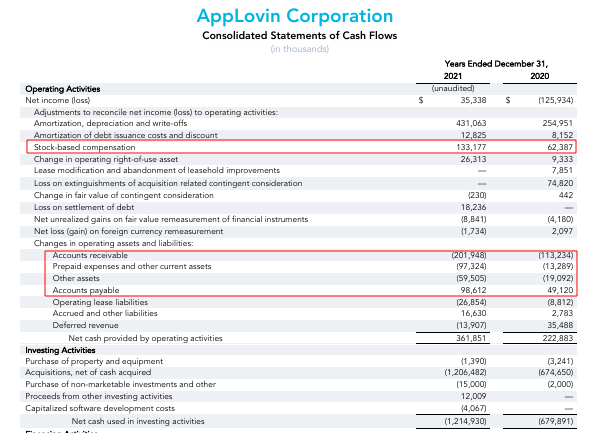

Being cash generative before SBC (and hugely cash generative before WC movements).

Let’s say