It has been a long time without articles here. Main reason is that I have been too busy. I feel the market has changed and accelerated, the time it takes for the market to switch moods and to price in several bits of information that lead to a specific set up has shortened dramatically.

I normally write about what I have been mulling for days or even weeks, and, in this market, prices jump around violently, which has made execution my principal concern. But luckily there is some stuff that doesn’t move.

I have been long INS since early 2019, it has been a painful two years. I have come back over and over this company to see why I got stuck into an underperforming stock for this long and whether there is any lesson to learn from it.

In early 2019 the stock price had embedded huge expectations, given how hyped the Apple card deal was and without any reliable information about how much would accrue to INS the range of possibilities was wide (to the upside).

The idea back then was that they would get a lot of license dollars (10% of which becomes maintenance forever) from the ramp up of the Apple card and that this deal with GS/AAPL not only validated the technology, but set a golden standard for competition, making the landing of new big issuing clients a matter of when rather than if.

Then bad things started to happen:

GS/AAPL sucked a lot of man power to keep up with the pace of features being released, which meant that onboarding new clients was subject to hiring more people and even then, maybe just one big client could be taken on in the next two years.

Wirecard was the second biggest client in 2019. No need to add anything. The Wirecard business was about multicurrency prepaid cards and the use case was travel in Asia.

2020 was a year “to catch up our breath”, meaning that onboarding clients was put on hold and the focus was to reinforce the infrastructure and hire new people to be able to manage a bigger operation. Coronavirus hit. India was badly hit (INS has most of their employees in India), WFH saved the operations but training and hiring was severely impacted.

Kabbage (second biggest client after the Wirecard bankruptcy) almost went under when lockdowns stopped funding. Lucky for them they turned to PPP loans (INS software had a lot to do with the swift change), that saved the company and it ended up acquired by AMEX. However the AMEX acquisition meant that Kabbage’s business would get wiped out as AMEX bought them for the SMB clients.

Despite all of this, the operating metrics have held up relatively well, but it is not the promised growth:

However… I think the company has a technological advantage and growth will resume. So here we go.

The Business

TL;DR section - you can skip the complicated descriptions and definitions and just read this teaser.

Corecard is a payments/software company, they have a software that provides de System of Record (SOR) and the connects and keeps track among all the payments participants. If you wanted to issue a card so people could buy stuff with it, you would need a software to track all the movement involved with card (similar to a bank account for a prepaid card) and, if credit, all the compliance and interest calculations (this is quite difficult stuff).

Corecard would sell that software to banks, or credit issuers or even resell it to others that would distribute it (Deserve) and make money. There are few players in the space, maybe 10-20 in the world that can do credit.

Corecard is not a new company, INS created VisionPLUS (which is used by Fiserv after they acquired First Data) and then rewrote to make it better, with more possibilities.

Ideally, Corecard would be like a Marqeta of sorts, disrupting the issuing side of the payments stack and partnering with fintechs to use their software. Marqeta doesn’t have a better product, just a better go-to-customer, Corecard has a unique product, but they spend ZERO in S&M. Herein lies the potential and the opportunity.

There are good articles explaining the business, like this from Richie Capital or some others on SA. Nonetheless I want to provide an overview of the business.

Corecard is their main subsidiary and only operating business.

We have a company with years of history (the management has many years of history too) that has been investing in a software to manage the card segment of the issuer bank and many other things like the system of record, while the motherboard (INS) sold down other investments and legacy businesses.

They have several lines of revenue all tied to the same “product”.

License revenue: This is a one-off item when they license the software to a new customer. However it doesn’t all show up when they sign a customer. Only when they deliver the software this revenue is recognized and the same customer can provide increasing revenues as it grows its operations and needs more licenses for new accounts. This is pure profit. It is to note that currently FD/Fiserv don’t want to license their software to new clients and only GPN/TSS are still open to new licenses.

Professional services: These are mainly customization of the software to the customer needs (this is usually required for every customer) and education in order to operate with it. Apparently this was supposed to be rather high in the beginning and then come down, however they have kept it stable and management refers to it as “almost recurring”, which makes me think part of maintenance is billed here.

Maintenance and support: This is recurring revenue. Aprox 15% of licensing revs become maintenance and support with time.

Hosting processing: This is the line everyone wants to grow, akin to SaaS revenues, this line provides a constant stream of money into the company. While in the licensed model they allow the banks to run their software, here all the operations take place on Corecard’s servers. They don’t break down how much is maintenance and how much is processing, but I’ve heard an even split is about right.

Third party: Pass through revenue related to the reselling of cards and hardware, it adds zero value.

The product

From 18Q3CC:

“CoreCard has developed a parameter-driven, real-time financial transaction processing software that's very flexible and easily customizable into a variety of products.

In simple terms, it maintains the relationships between an account. An account can be a person, a company, a vehicle or any number of things – and, with a currency. And the currency can be dollars, rewards, gallons of gasoline or any number of things. So that software is generally productized most often around what's commonly called a card management system or an account management system that provides account personalization and lifecycle management of a credit account.”

In 2019 Q1CC they indicate that the software is a rewrite of “VisionPLUS was our previous product that we had developed at PaySys over many years and we saw at the First Data and this product is a spin-off. I can call it that, it's a rewrite that we think is superior.”

This program is not written in COBOL, as it’s the banking software state of the art, but in C+. This makes it parameter driven and more flexible, hence it can adapt faster to new demand from customers. As long as the software is safe the technology is superior. They are the only ones that can do real time processing (Not sure how desired this actually is what extra price a customer would be ready to pay for it)

2019 Q2CC: “real time environment is simply what everybody wants. You can't do it with the legacy systems. You can pseudo real time, which is what they're doing, but people want real time. That's the only way you can do certain things.”

The fact that this software powers such a critical infrastructure makes relations with customers sticky, although not inmutable.

As to what position they are within the industry (2018 Q3CC):

“The other main leg of the business is hosting processing, using the same kind of products I just described. This would be what is traditionally called “processing,” similar to what (TSYS) and (First Data) provide for their issuing business.

And don't get this confused with their acquiring business because they have acquiring business also, and that is merchant acquiring. First Data’s heavy in this and pushes it all through to merchant point of sale terminals.

Remember, we work from the issuing bank side, the one who provides the credit or card or loan or check or prepaid account, not for the merchant-acquiring side that accepts the card for purchase. The merchant sends the request for authorization to the issuing side, and our software takes care of that. As an aside, we could do the acquiring also with our software, the way it’s architected, but is not really our current strength, so we're not pursuing that.”

Now a brief word about how electronic payments work. A simple credit card transaction can be processed through many different platforms such as e-commerce stores, wireless terminals, and also mobile devices.

The whole process of swiping the card to the receipt produced takes place within few seconds.

Stage 1 – Authorization (Corecard would be the one that receives and handles the ask for authorization)

In this stage, the merchant obtains approval for payment from the respective issuing bank.

When the cardholder buys a product or service from the merchant then he presents his credit card for the purchase.

On the point of sale (POS) the merchant swipes the credit card and it sends the credit card details to the acquiring bank.

The acquiring or the merchant’s bank forwards the details of the credit card to the credit card network.

The credit card network i.e. Visa, MasterCard, etc clears the payment to ask for authorization of the payment from the issuing bank. The request for authorization includes the following details:

Credit card number

Expiration date

Billing address - for AVS validation i.e Address Verification System

CVV of the credit card

Amount of money to pay

Stage 2 – Authentication (INS would be in 1, 2 and 3)

In this stage, the issuing bank verifies the consumer’s credit card.

The credit card network sends the authorization for payment to the issuing bank.

Then the issuing bank checks the number of the credit card, amount of available money, the billing address and finally the credit card security code.

The issuing banks send the appropriate response to the merchant through various channels - credit card network and merchants bank.

Then the merchant receives the authorization and the issuing bank will place a hold on the purchase amount on the account of the cardholder.

Hence, the sale completes when the merchant provides a receipt to the customer.

Stage 3 - Clearing and Settlement (INS job is done at this stage)

The clearing and settlement stage occurs simultaneously. In this stage, the transaction is published on both merchant’s statement and the cardholder’s billing statement.

The transaction details get posts by the issuing bank to the account of the cardholder. Hence, the cardholder receives the billing statement and it pays the required bill.

Infographics:

If you made it here you deserve the good and interesting stuff.

What’s next?

Kabbage - AMEX

The acquisiton of Kabbage raised a lot of questions about what the business with the company would look like after the acquisition, a bit of a double edged sword at the beginning as Leland said during the 2020 Q3 CC “[Kabbage] successfully sold their company to American Express, and our contract has been assigned to AMEX. I guess that means we can now count AMEX as a customer. Seriously, this illustrates the kind of customer we want to partner with. I don't know what future business will look like with AMEX. And the fourth quarter will be very light compared to past quarters with Kabbage”

In the 2021 Q1 CC comments were more positive “Similarly, we have started processing loans for American Express, but minimal revenue was recognized in the first quarter and it's still too early for us to determine the degree that this new customer will impact 2021 revenues.”

Also AMEX had some job openings that mention corecard. (That is a cached link, I have saved the page, hope it works by the time you are reading)

So wherever this goes, it seems INS has foot into American Express and they are not shutting down Kabbage.

From the 2021 Q2 AXP CC: “But I think one of the big things that we've done, obviously, is the Kabbage acquisition. And just last month, we launched the Kabbage checking account, the working capital, cash flow analysis and so forth. And what you'll see ultimately is that Kabbage platform being the landing point for our small businesses. And the way you want to think about this is fintech with scale.

And so when you think about Kabbage, which is a pure-play fintech in the small business space, and you think about American Express and the small businesses and you combine that together, you have a fintech at scale, not a fintech growing at scale, a fintech growing from scale, from scale with the balance sheet. And so that has always been the vision of Kabbage. We've made -- as you bring Kabbage into the bank holding company structure, you have to do some other things to future-proof it, if you will, and that's what we've been doing. But that's what you will see. Ultimately, what you will see is a fintech with traditional bank scale and a very strong balance sheet, and we'll continue to add products as we move along on to that platform. And that was the vision, right?

I mean we see a lot of other people out there doing those kinds of things. But to be able to do that at scale from the get-go, I think, is a big win for us. So that's a long -- that's the vision in the medium term here for Kabbage, and we just launched that platform from an Amex perspective just last month with those other products on it.”

I like how this article explains how Kabbage would fit into the Amex complex, and although Amex is not giving any business loans on the website, they probably are moving this to the Kabbage platform.

Apple BNPL

Boomberg announced that Apple would be launching a BNPL service through Marcus. Goldman Sachs would be the one buying the credit from whatever card was used in Apple pay and offer the installments.

This is something Corecard could be doing, but is pure speculation at this point. To add to this wonderful nugget:

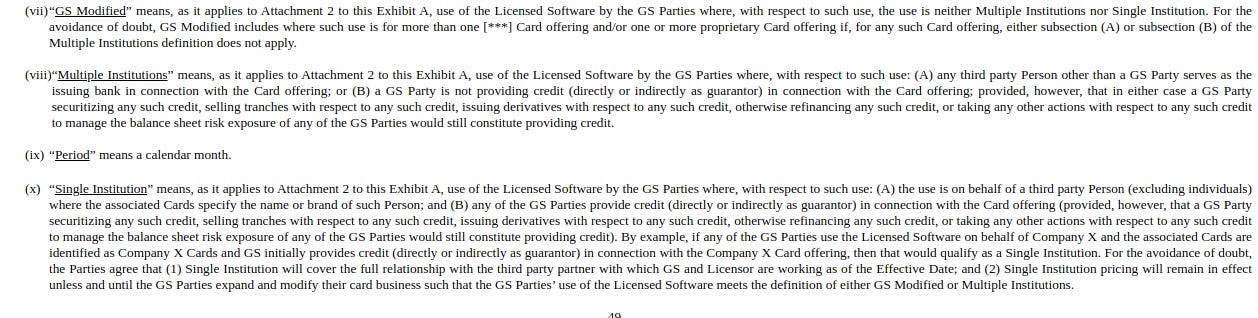

I want to get your attention to these definitions in the software license and support agreement between GS and Corecard that contain a use case for their software (GS modified) that would be the Apple BNPL situation, this would trigger further license payments (Albeit we know nothing about pricing of that category).

GS and the GM card

What we do know is that Goldman Sachs will get the General Motors card business and this is for sure another “Single Institution” which will trigger the same license stream as the Apple card did. This license will be felt in the latter part of the year.

Deserve

Deserve is a processing costumer of Corecard and is currently powering the card offerings of:

Besides BlockFi being probably Corecard/Deserve powered (management has mentioned a credit card that uses crypto) the others might be powered by Marqeta instead. Although Marqeta had no business in credit, they recently announced their credit platform and partnering with Deserve. INS management has acknowledged this relationship as competition.

If not, this shows that there is life in the processing side of the business.

If/when some of these projects show up on INS financials the company should do well.

INS is trading at around x6.5 EV/S (part of it being license, which should command a lower multiple) and x18.5 EV/EBIT at normal margins.

They expect to keep growing in the future.

Leland said that at $40 per share they think the company is at the lower range of fintech valuations.

They bought back stock at $38 during Q1.

GS considers them a key partner.

Maybe they should just burn through S&M acqui-hire personal in the US, go for every deal, add some customer support… and they would jump to x20 forward sales. That is not gonna happen under Leland’s watch. But I think the company should be worth more in 1 year, and more even so in 2, 3 years.

To me it is not that much about multiples, relative valuation of DCFs… When I look at a company, at what they do and what they may become I come to an enterprise value in my head, and knowing what Corecard is able to do, the list of clients they have and their future possibilities… I come to an order of magnitude higher price than this.

If I am wrong I will sell my shares and assume the mistake, it is now or never for INS.

Very good article. What are you thoughts now that $CCRD appears that will loose Apple Card business?