Dwelling on the SPAC phenomenon

Pre-deal SPACs

The general strategy of buying a pre-deal SPAC common share is benefiting from a potential good deal with the downside protection of the redemption at NAV. Obviously, the problem is the opportunity cost of having your money tied there until a deal lands or the SPAC terms out, as well as losing the premium to NAV paid - if any.

Arbitrageurs buy shares below NAV to benefit from the ROI until redemption with the optionality of being exposed to a “hot deal” that makes shares rise sharply.

Speculators/Investors buy shares above NAV to get exposure to one of those deals with a fairly limited downside, in the end, it is a bet on the promoter. More aggressive speculators may even purchase warrants instead of commons, which go to zero if no deal is closed.

Although interesting, a generalist like me cannot apply neither of these strategies, I don’t fancy buying SPACs at a premium to NAV nor have the capital to implement an arbitrage strategy. However, I am enough of a speculator to fiddle with something similar, with unknown results, but good enough odds.

Before common shares and warrants can be traded on a certain SPAC, there is (normally) 52 days of trading of SPAC “units”. Those units include a common share and may or may not (like the 3 biotech SPACs referenced below) include portions of warrants, whole warrants for a fractional share, rights and other kind of exotic instruments that become separable after 52 days since IPO. Normally, the shittiest the SPAC, the more “incentives” for investors it has. The units keep trading after those 52 days, but now the price of the unit comes as a function of the price of the common and the warrant.

For example, if we have SPAC “Climate Change Gives Bad Vives Bro XIV Acquistion Corp.” with units that include one common and one half of a warrant, the price of the unit will be:

Price of the unit = Price of a common share + 0.5*Price of a warrant

If any of those three prices move, arbitrageurs will keep the equation balanced. The separation tends to increase the price of the units, as there is a certain market for pre-deal warrants. If they are too cheap (say $0.10 per warrants) asymmetry is huge, and they become a good YOLO bet. That is why pre-deal warrants have a floor of $0.40-$0.60 (Pure empirical numbers, no reason for this more than risk appetite I guess). That new market of speculators buying warrants is enough to push the price of the unit up, while the commons are still good enough for arbitrageurs and investors.

SPAC units

Again, this is very cool, but how does it help us? Well, as a result of the SPAC boom and sponsors capitalizing on free money, many recent SPACs (whose units are not yet separated) trade at a discount to NAV (ie: below $10).

You can buy a unit at $9.92 that includes the common and one third of a warrants, wait the 52 days or less to separation and play both strategies at the same time. After a couple of months of buying that unit at a discount three things can happen:

Separation gives you a $0.20 per unit from the warrant (warrants at $0.60) but common shares drop the same or even more than that and you end up holding the warrants and a common that should provide (at least) some small upside until redemption (max. 2 years). Congratulations, you are a SPAC baggie, but at least you’ll make your money back waiting, so not really terrible, is it?

Separation gives you a $0.20 per unit from the warrant (warrants at $0.60) - or whatever price it trades at. And the common goes to a a certain discount to NAV - or even premium to NAV - such that you can sell the common and get the money you put on the units back. At this stage you could sell the warrants too and realize a small profit, but it is funnier to become a warrant speculator for free. ROI of ∞%.

Your SPAC announces a decent deal before separation (ie: ARYB.U) and you make money as warrants increase their value markedly once the feeling is that the deal will get through + commons trade at a premium (if deal is decent).

None of these options is terrible and an investment in units at a discount to NAV should be deemed a sensible trade. Luckily, we have so many SPACs that we can try to choose those that have a higher likelihood of avoiding situation 1 and thus become a warrant collector.

The first strategy would be to buy units at a discount of a very good sponsor (Ackman, Chamath have all the mojo nowadays), but these really famous sponsored SPACs don’t trade at a discount at all. (Social Hedosophia III traded at a 10-15% premium to NAV before the Clover Health deal was announced, now it trades almost at NAV, so speculators got fried on this one)

The second option is trying to find a good sponsor that doesn’t appear in CNBC all the time. I personally like True Wind, with their second SPAC, TWC Tech Holdings II Corporation. Their first SPAC, Nebula, merged with Open Lending. Based only on that deal, it is an option to consider. Some other sponsors could be Fertitta with Landcadia Holdings III the first SPAC merged with Waitr Holdings (I know, I know but on the deal it popped!) and the second with Golden Nugget Online Gaming, this one hasn’t closed yet, but it popped on the deal and even it is Fertitta selling GNOG to himself which is atrocious, it is good enough for a pop.

The third option:

BIOTECH - Doubling down on volatility.

First of all, it is very curious to see how three of the last biotech focused SPACs have NO public warrants as part of the units. Interestingly, ALL of them trade at an arguably substantial premium to NAV - which for early SPACs, for simplicity, we will calculate as $10 per share.

BCTG Acquisition Corp - Sponsored by Boxer Capital, a firm based in San Jose, California. Worth checking their website to go over their ventures.

FS Development Corp - Sponsored by Foster Capital, a rather big investment firm. It has many investments in their portfolio. Which announced a deal TODAY. You are not going to wait 2 years for these to find a target it seems.

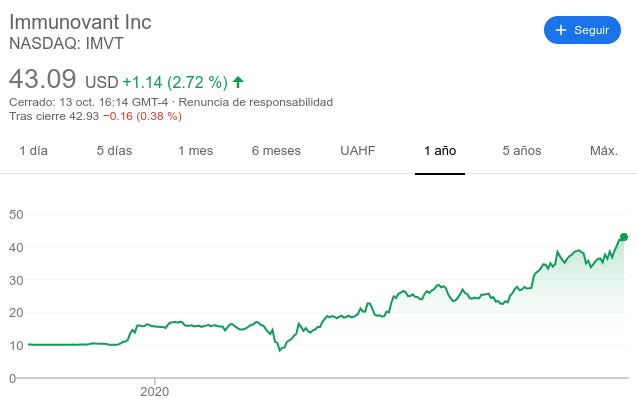

Health Sciences Acquisitions Corporation 2 - Sponsored by RTW investments. No wonder why this one trades at a premium to NAV, their fist SPAC took Immunovant (NASDAQ:IMVT) public. A clinical-stage biopharma focused on autoimmune diseases.

This is what some positive clinical results can do to your SPAC:

There are other two biotech focused SPACs, and these have one third of a warrant as part of their units:

HighCape Capital Acquisition Corp. - The sponsor, HighCape, is a small fund out of NY, all I’ve found are private deals, either they are very good or very bad. SPAC size is not big, and with SPACs the bigger, the better. The units have traded close to $10 for some days, even if the sponsor is mostly unknown, the units should not trade at a discount to NAV after separation, if the above examples can be any guide.

CM Life Sciences Inc. - The sponsor, Casdin, is one of the biggest biotech funds and considered quite good by the investment community, I know them from being a BLFS partner and a big boy, others would be RTW and Perceptive. The units traded at $10 for a day, and I think it would’ve been an incredible buying opportunity, with other commons trading at a premium to NAV, the units at $10 had a high chance of being free warrants.

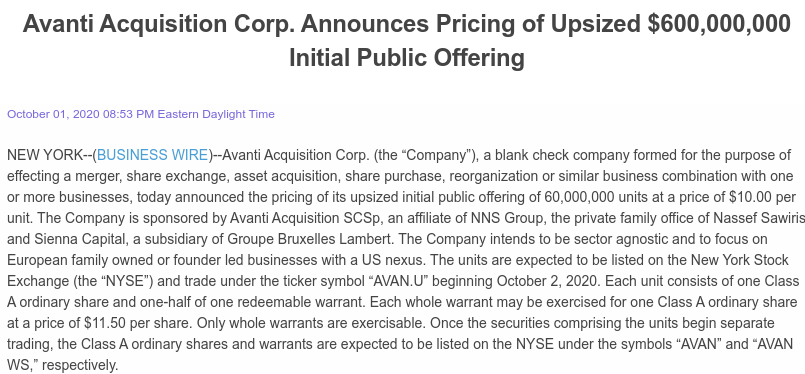

Another interesting SPAC for some units below NAV:

This one is interesting, as its focus is on “European family owned or founder led businesses with a US nexus”. I like the setup as a way of capitalizing on the US / ROW multiple disparity, even if the company operations are located in the US.

It is controlled by Nassef Sawiris, which, honestly, could be a huge positive or a stark negative. With SPACs it really comes down to the deal.

Thanks for reading. Feedback is welcome.