Inspired Entertainment

The business

To understand the company we need to look into the segments and disentangle each one of the lines of business as they are gaming related, but radically different.

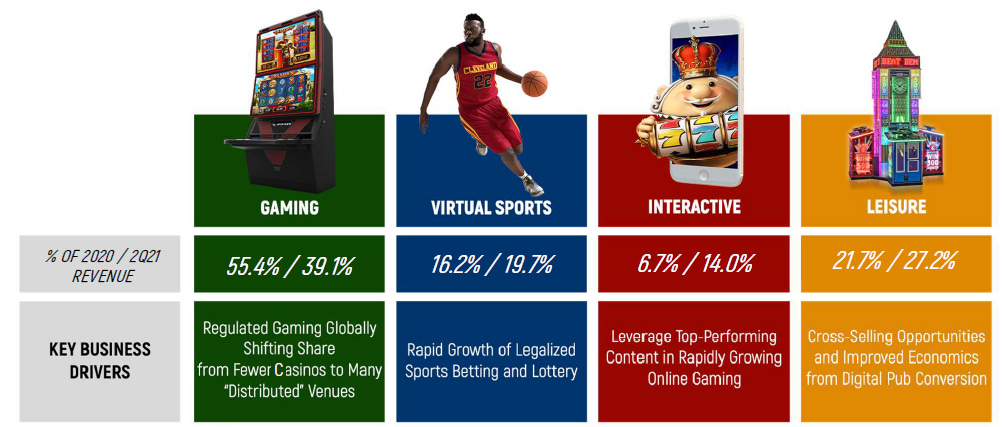

Segments – newly reorganized in Q4 2020, per the Press Release:

Gaming: Gaming machines located in UK licensed betting offices ("LBOs"), casinos, gaming halls and high street adult gaming centers ("AGCs")

Virtual Sports: Retail and Online Virtual Sports

Interactive: Slot and table game offerings from our Gaming segment as well as interactive-only content via our remote gaming servers

Leisure: Digital and analog gaming and amusement machines located in UK pubs, bowling alleys, motorway service areas ("MSAs"), bingo halls and leisure parks.

Gaming revenue is the money the company makes through the gaming machines it sells and leases. Most of the revenue is from revenue sharing contracts, meaning that INSE gets a percentage of the machines’ gains. Thus, this line of revenue is very impacted by number of people betting in the machine (foot traffic into the betting shop for that matter) and the average bet per person.

Slots machines or fixed-odds betting terminals (in legalese) are a high margin business. These are placed in betting shops, casinos, pubs and basically anywhere where is allowed and has high foot traffic. The main upfront cost for the operator is obviously acquiring the machine. Once it is set, it becomes a cash cow.

Operating costs are low and the main issues revolve around tax duties and regulation. Machines need replacement, as new shinny terminals (digital nowadays) attract punters more successfully, nonetheless, I estimate the economic life of the machines should be around 10 years.

This was - and still is, although with a lower share of total revenue - the main business when the company de-SPACed in 2017. The acquisition (Gaming Technology Group) they did in 2019 was of a competitor in this area too.

It is a slow growth, stable business threatened by regulatory clampdowns on slot machines. Although stable to decreasing in the UK and Europe, INSE’s machines seem to be selling well in the US. It is not a capital light business, although the machines have probably a longer useful life than amortization periods suggest, regulatory changes can make the machines obsolete or cap the bets and thus cap the profits. This was the case in 2019 as betting limits went from 100 pounds to 2 pounds, which forced a reorganization of the betting shops and lowered income per machine.

Virtual Sports segment is about people betting on a “virtual” game. It is not betting on a FIFA game with two human players competing on a PlayStation. Pure virtual game as in the game is developed by an algorithm and the outcome is determined in an unbiased way, but with fixed odds.

This way of sports betting saw a surge in adoption with the first lockdown propelled by the absence of real sports. For INSE costumers, it is a good way of providing 24/7 sports betting (although without the things that make sports betting great, like the possible edge that real sports offer gamblers or the emotional aspect of rooting for your team.)

They make money licensing their technology to operators getting an upfront fee and a revenue share based on net revenue to the operator.

In the post-Covid world, online betting in virtual sports has decreased slightly and is being offset by retail venues.

Interactive segment was formerly hidden in the old reporting. It is a translation of the slots games the company has developed for the physical machines into virtual games served to operators. This is basically an online slots gaming business growing 70% YoY and 11.5% QoQ in the last quarter against tough comps from the lockdown period. Again, contracts include a participation on the net wins of the operator.

I personally see this segment as a hidden gem. It is not Big Time Gaming at all, but at a run rate of $24M and decent EBITDA margins – around 60% (Not as high as the 90% implied by the PR on the Big Time acquisition and taking out INSE corporate costs). Big Time was bought by almighty Evolution Gaming at $260M and $276M in earnouts for $40M TTM revenues.

Leisure segment is just physical slot machines but placed in pubs, oil stations and leisure parks. The hardest covid hit of all the segments.

Management

A. Lorne Weil - Executive Chairman

Being INSE a former SPAC, he was the Chairman and CEO of Hydra Industries Acquisition Corp and then kept the Chairman role in the merged company. I like he was former chairman and CEO of Scientific Games, which means he knew the sector at the time of the merger. Although the performance post deSPAC was bad, it was still better than his next SPAC, Leisure Acquisition Corp, that after several extensions and a mere $13M in the trust merged with… Ensysce Biosciences, a biotech desperate for a listing. It holds the title of the worst performing SPAC that closed in 2021 with a cute minus 70%. YLTSI.

Brooks Pierce - Chief Operating Officer and President

He has experience in the sector, with some years at Scientific Games and was promoted to COO in 2018 after Luke Alvarez, founder of INSE resigned from his role. I think he is a valid operator.

Personal take

I tend to think about the company as a mix between a cash generative but rather stale business (slot machines) and another part (Virtual Sports and Interactive) that has good economics and certainly higher terminal value than the slots machines. If Virtual Sports finds its place in the US betting shops and is able to grow and/or the Interactive part keeps growing, the company is due for a rerating.

However, there are quite some moving parts in the financial statements as well as in the business. First, the 2019 acquisition was being digested when Covid hit and in early 2021 reporting segments changed. Since Covid this company hasn’t had a normal quarter. The third quarter of 2021 will be the first without restrictions and – arguably – with some pent up demand from gamblers.

This is a company beneficiary of reopening but with a strong foothold on iGaming.

Financials and capital structure

Until now I have been focusing on the operating side of things, but the financial structure of the company is… interesting.

As we lack normalized TTM numbers, I am going to work with what a post-Covid normalized EBITDA looks like, in the last conference call (2021 Q2) management stated:

The formal EBITDA guidance for 2021 Q3 is $28M-$30M. If we naively annualized it, we would get to $112M-$120M. I think they can get there, but let’s use $100M as a figure that is comfortably ahead of $80M.

Now that we have an idea of what the business can do without lockdowns, let’s go over the issues.

Issue number one – the debt

Debt is high. Long term debt (recently refinanced with lower interest) stands at around $320M (234M pounds). Debt is bigger than the market cap – $280M at $11.5 price per share.

It is slightly above x3 Debt/EBITDA, so no wonder the equity is volatile.

I personally don’t mind debt in the businesses I invest in as long as it stems from sensible capital allocation. I think INSE is carrying too much leverage and it should start pay down debt when the lockdowns are over, but this level is manageable if the business performs as expected.

Issue number two – the warrants

Although not really an issue per se, it impacts valuation and the stock dynamics, so I think it is worth mentioning.

Being a former SPAC this company comes with warrants. There are around 23M shares outstanding (non-diluted) and 9.54M warrants, with strike $11.5. Although it is not as massive as recent broken SPACs – BMTX has x2 the number of warrants compared to the number of common shares, and I am sure some of the new high redemption SPACs will have a high ratio too – the amount of warrants is quite sizable and, I believe, a drag for the price to go up much beyond the strike price.

These warrants expire in December 2021. If the price of the common is below the strike, the warrants expire worthless and make upside much more attractive. If the price is above, most of the warrants will convert and the company will see an infusion of up to $110M, deleveraging the company and removing a lot of downside and some upside.

Valuation

I will take a multiple approach, I love multiples. My process normally starts with getting a qualitative idea of the business and then figure out how much it should be worth, then the multiple tells me what the market is ready to offer for it. It is up to you to decide whether the current valuation is too much, too low or maybe just fair.

Historically the Capex has been around 6-7 M per quarter, let’s say $25M per annum . I prefer round figures for made up numbers, so $50M of FCF.

Conveniently, you just need to x2 the EV/EBITDA ratio to get the EV/FCF. Attractive IMHO for a company with a rather mediocre business (slot machines) and two really valuable segments (Virtual sports and Interactive).