Intellicheck - IDN

HGARP in times of SaaS craze.

The business

IDN provides verification of fake ID’s for all North America issued ones. Basically it scans (in 2D vs 1D for other uses of the barcode) driving licenses and then checks whether the scanned barcode has the info the license says it has.

They are the best at what they do, no other company has come close to the level of accuracy IDN achieves. The product rolls out easily as it doesn’t require new hardware on the retailers side. They also have a web product and can get people onboard just logging on the site, but it normally takes a couple of weeks to integrate the software in the retailers’ systems.

The customers

Although the user is normally a retailer (it can authenticate online asking for a picture of the ID) the customer often is a financial institution that extends credit (or whomever extends the credit) and wants to rule out phishing of the person submitting the application.

Once the financial institution is onboard they roll out the product quite fast. Some institutions require the use of IDN’s product for retailers to get their card program (more on the CC clips). Sometimes it is used to review the applications before getting the credit card.

Alternatively, some big retailers that extend credit on their own work similarly to financial institutions. It should be noted how the software auto-populates the credit application once the scan has been successful, which adds value and exemplifies the smoothness of the product.

Another use case is for restricted-age products, this market is arguably smaller and, let’s say it, some sellers won’t spend money to stop it. They have a flat month rate for this product and per-scan fee for the others.

However, the product originated and was mainly used for checking identities at law enforcement agencies and military bases. If you check the biographies of some board members you’ll se a pattern emerging:

This takes us the next point.

The advantage and the moat

IDN has reached such proficiency at scanning ID’s thanks to its connection with the DMV and AAMVA. There is no incentive to work with someone else, as this information is quite sensitive. Competitors have to reverse-engineer the barcode magic.

I’ve seen this pattern in some US companies. A private company providing a unique service to the public sector, some kind of entrenchment between both (board and/or employees) and the free pass to profit from that connection in the private markets. I call them the good GSEs, also EBS (This one more of a toxic relationship that virtuous). H/T to @hareng_rouge on that article.

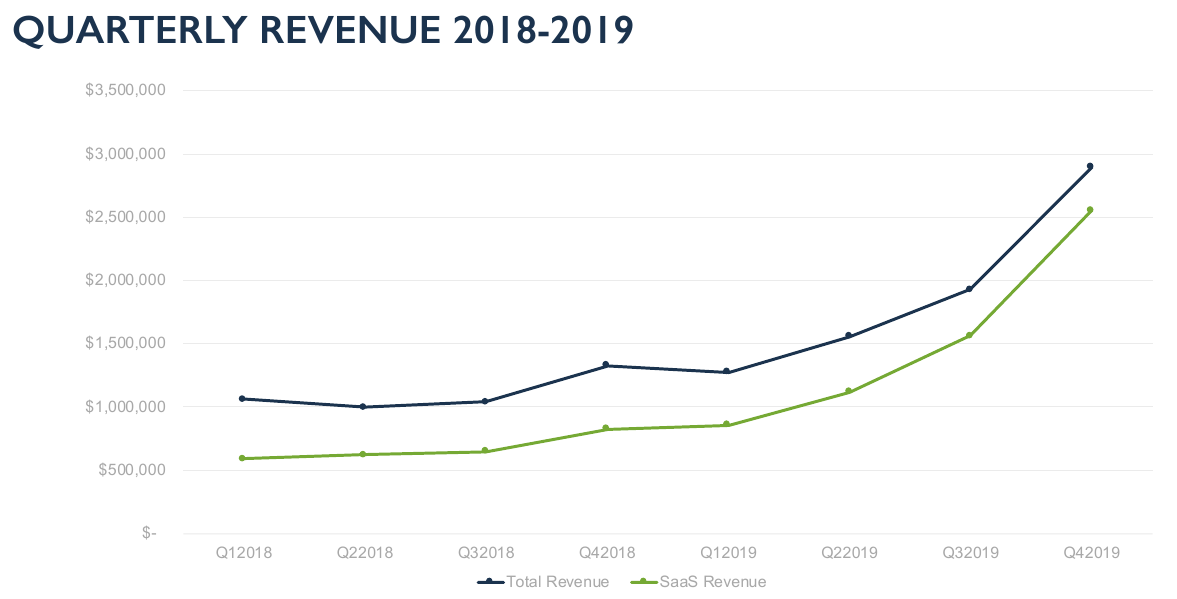

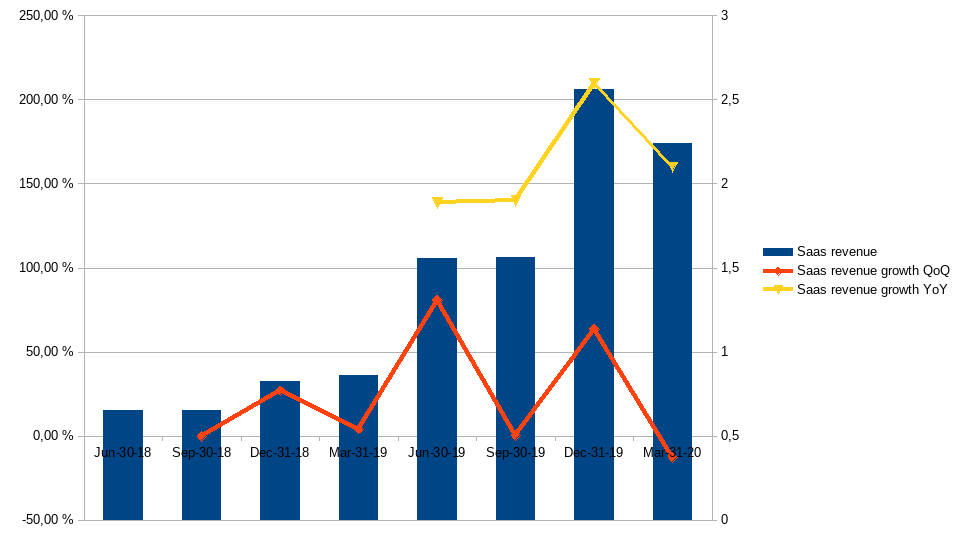

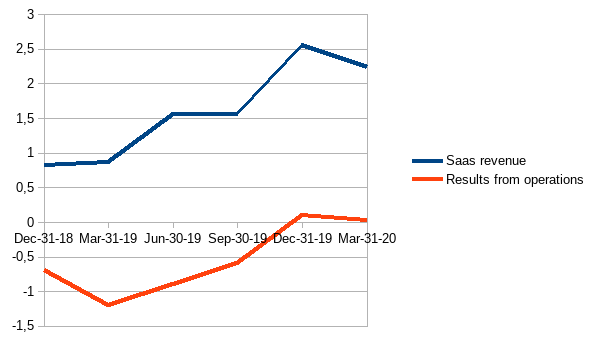

The valuation

Plotting the growth:

Operating leverage does exist (Gross Margins 85%-90%):

Trying to estimate 2020 revs; assuming rough conditions for the reminder of the year and baking in what we now (Q1 SaaS revs + Q2 guidance) I have them doing 8.5$M of SaaS revenues, EV with the recent placing and at $7.5 price it is around 15x EV/S. I am not including the NOLs.

They have won a couple of big clients recently, so if things normalize a bit, we should see higher revenues.

Final notes from last CC:

“I am pleased with the SaaS numbers that validate that we are on track with our plan for Q1. If you recall, we said that 21% of annual scans coming in Q1, 23% in Q2 and Q3 and 33% in Q4. So a 12% drop in a typical quarter would be expected. We had great momentum leading into mid-March, and I believe that if we hadn't been impacted by the pandemic, then we would have seen an increase in total SaaS revenues quarter-over-quarter.”

“Financial services company #1, a top 10 bank, brought live a 10-member consortium. This is a newly won client for #1, and it is interesting to note that #1 made a condition for them getting the card program to manage their own usage of Intellicheck's Retail ID Mobile to authenticate IDs as a first step of the credit application process. I think this, again, shows that banks can use the fraud fighting power of Intellicheck to gain a competitive advantage and provide better rates on their credit card programs and induce prospects to switch banks for better rates.”

“The new nationwide stay-at-home orders, however, do not mean 0 revenues. We have a growing online business with 14 retailers, allowing customers to apply for credit on the website and multiples of our financial services companies are using our web tools and the call centers for everything from card applications to account changes. All of our clients, even those on a per scan model, have minimum unpaid payments”

“Given the current market and what we know today, we are hoping to achieve about 60% of the SaaS revenue in Q2 that we had in Q1. From there, we anticipate things will begin to ramp back up as more retailers and restaurants open up and we see increased transaction activity.”

Nice post, Rodrigo! Just to add some context behind their margins, IDN pays 12-15% of first-year revenue as commissions to their salesperson and recurring 1% subsequently.

vested. They won Amex, Key Bank and Fifth Third Bank, I believe.