Minim, a call on the former Dyn team.

Minim, a call on the former Dyn team.

Zoom Telephonics Business

Zoom has been around for a long time - they still have dial-up modems - during all their history, Zoom has commercialized Internet access and other communication products (cable modems and gateways, mobile broadband modems, wireless routers, Multimedia over Coax (“MoCA”) adapters, Digital Subscriber Line - ADSL rings a bell?).

Summing up, nowadays they sell home retail Wi-Fi networking devices, mainly cable modems, network adapters, routers, range extenders, and access points modems, and dial-up modems. Probably growth will come from the mesh Wi-Fi market.

Of course, this is a lousy business, with no pricing power and thus scrambles to outsource production to the cheapest country posible. They have moved production from Boston to Mexico to China to (thanks to the tariffs) Vietnam.

Just the retail market

Everyone with Internet has a modem, a cable that connects them to their ISP network and router Wi-Fi… But nobody buys it themselves.

The ISP commercial market makes most of the networking devices sold and under use. While some companies sell to the likes of AT&T or Comcast, Zoom’s focus is the customer that would rather buy their own modem than use the one provided by their ISP. There are good savings in buying your own modem and stop paying the ISP for the one you borrow them, if you can make ISP to cut that concept from your billing (I think Charter doesn’t).

If Zoom were to strike a deal to sell into some of these Tier 1 ISPs they could get a higher order of magnitude scale and sales, but so far, they are constrained to that nerdy segment of the market.

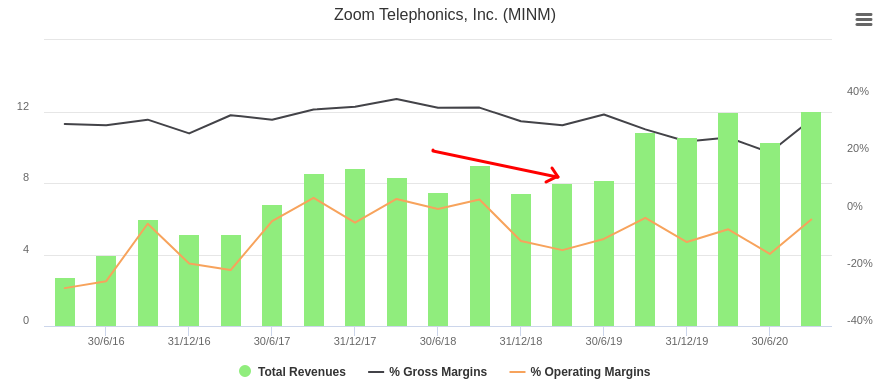

Before you look up the chart, I’ll do it for you.

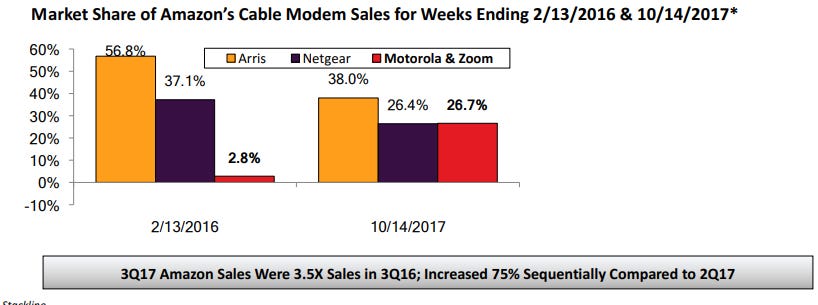

That pop in 2015/16 is the company reaching an agreement with Motorolla to sell modems under their brand (Zoom’s brand doesn’t appear in the packaging). Since the selling to Google, Motorolla is just a brand shell with no real business and certain goodwill from the brand.

Until Zoom struck the deal, Motorolla was selling their modems with the dual brand Arris/Motorolla. Whatever Arris did, Motorolla didn’t like it and sought a new partner. Zoom then struck deals with retailers (Target, Amazon…) and sales grew at a fifty percent clip. However, Arris kept the Amazon history and goodwill from their years with Motorolla, so all the favorable opinions about the Moto/Arris modems went to the standalone Arris modems. Those dynamics entail that Zoom didn’t get all of Arris’ business, just a bite.

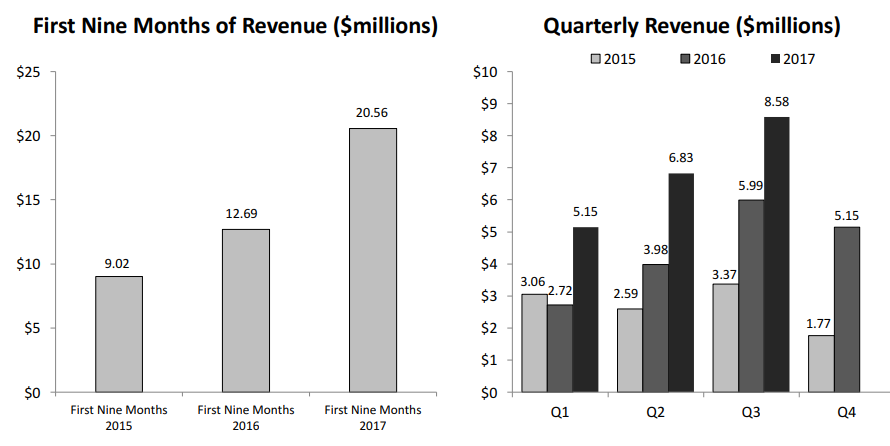

All from 2017 Q3 presentation.

Motorolla seems happy with the partnership as in 2016, it agreed to extend its brand license with Zoom beyond cable modems to include all home Wi-Fi networking devices on a global basis. In 2017, Motorola further agreed to add cellular and DSL modems and gateways, MoCA adapters, and cellular home sensors to the agreement.

They deal was struck for 5 years and in early 2020 they agreed to an extension until 2025.

The issues

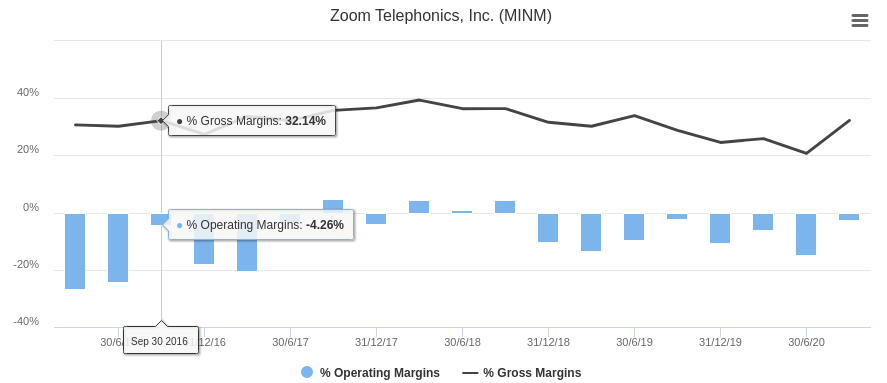

If you looked at the chart, after the 2016 pop, you might be wondering what that 2018/9 debacle was about.

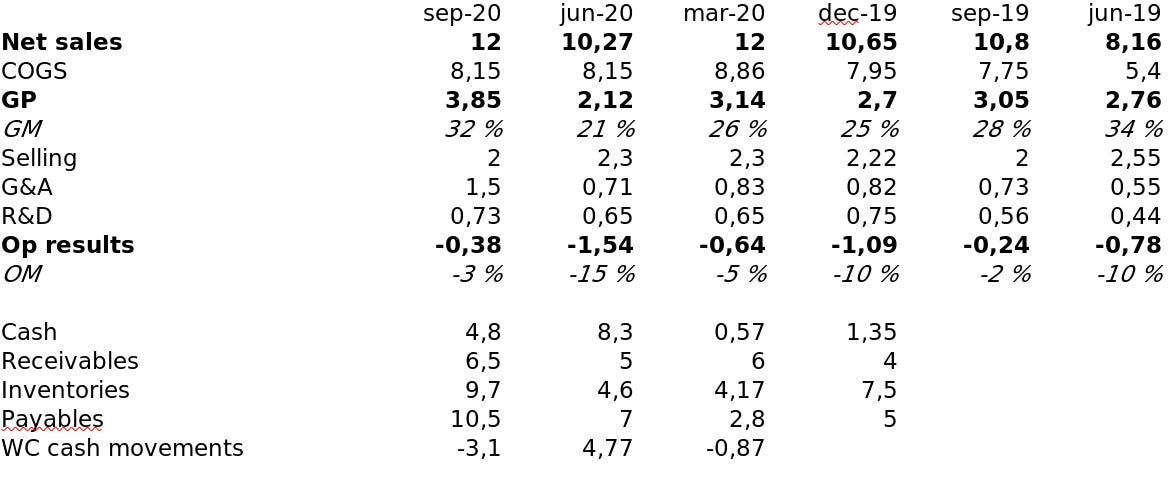

Zoom business is not prone (unlike other superior business models like $TRIT) to high margins, here you can see the evolution in the last 5 years and your first cue at the share price debacle.

Once the Motorolla deal got traction and Zoom reached some scale, they could boast slim positive operating margins. Then Trump tariffs hit, the tariffs ate all of the positive margin and some more. The company reacted first trying to pass the cost through to the consumer, but modems are not insulin and sales took a hit.

Since then, the company has worked to switch production to Vietnam, however not without challenges as some components are still sourced in China and have to pay the tariff to get mounted and shipped into the US. The company says that the transition will be complete by the end of 2020. This is what the company has to say about the future of costs (2020Q3 CC):

We continue to reduce the impact of tariffs as we moved our manufacturing to Vietnam, which as of the end of the third quarter represented approximately 98% of total production. As a result, our gross profit margins improved on a sequential quarter basis, increasing from 20.7% in Q2 2020 to 32.2% in Q3 2020.

During the third quarter, we decreased our reliance on airfreight to ship our products from Vietnam to the U.S., which reduced our total freight expense as a percentage of sales by 36%. We will continue to utilize airfreight only if necessary to meet demand and to drive continued growth.

On a year-to-date basis, net loss was $2.6 million, including $2.6 million in tariffs. Excluding these tariffs, non-GAAP net income year-to-date would have been just over breakeven. We also incurred $1.4 million in temporary supplemental airfreight expense in the second and third quarters of this year. Excluding both the tariffs and the temporary supplemental airfreight expense, year-to-date non-GAAP net income would have been approximately $1.5 million.

I am comfortable using $2M as a net income run-rate, as it equates to the 4% margins they enjoyed in their best times.

The transaction

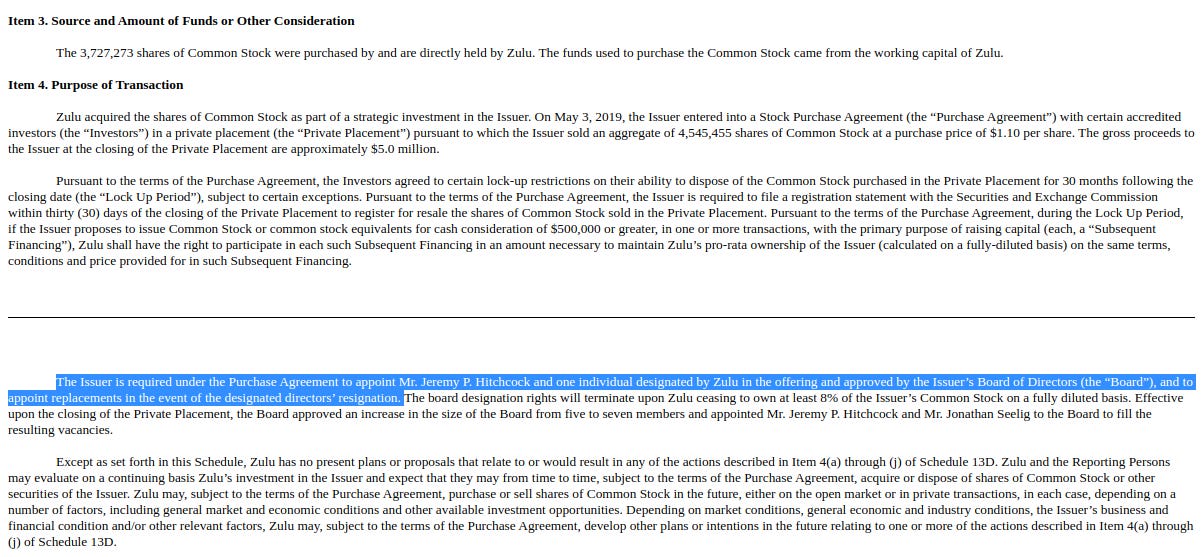

Come May 2019 enters into the story Jeremy P. Hitchcock & co. - Jeremy P. Hitchcock, Elizabeth Cash Hitchcock, Orbit Group LLC (“Orbit”), Hitchcock Capital Partners, LLC (“HCP”), Zulu Holdings LLC (“Zulu”) - with this 13D. They acquired 23.1% of the company thanks to a private placement the cash strapped Zoom needed to support the loses and the working capital requirements.

Mr. Hitchcock must like the business, because by October of this year the group owns more than 50% of the shares, buying out former directors and preparing the merger with MINM.

This is the end state of the new ownership in the business (Last 13D I promise)

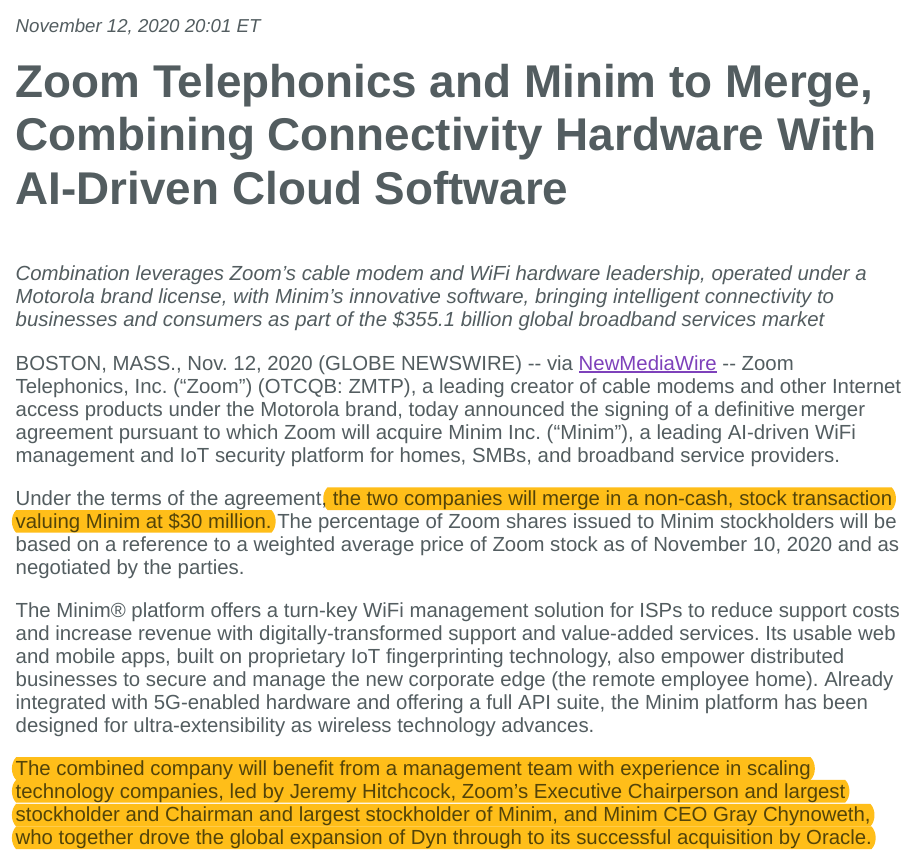

In November this year, the merger with Minim is announced and it closed in December. From the PR we can see how Mr. Hitchcock has decided to merge this two companies, it is clear by now this is a one man show:

So, who is this guy?

Dyn

Mr. Hitchcock founded and led Dyn until 2016, when he stepped down as CEO shortly before the company was acquired by Oracle. From the link:

“Dyn, which is privately owned, employs 400 people, with three-quarters of them in New Hampshire, mostly in Manchester, though it also has a small office in the Hanover area. It has an option to expand at its current location, Hitchcock told NH Business Review on Tuesday.

The company said it has grown 70 percent in the last few years and expects to surpass $100 million in annual recurring revenue later this year.”

Dyn offered DNS services as well as internet optimization tools (ie: allowing you pages to load up faster) that came to fame in 2016, when it suffered a DDoS attack on Dyn servers that affected a lot of big companies. Shortly after the attack Oracle announced an agreement to acquire Dyn, for an undisclosed price that was reported to be north of $600M.

Whatever the price, Mr Hitchcock got enough to retire and become an angel investor. This is what he is at from his Linkedin:

“Jeremy’s focus is now on Minim, an AI-driven WiFi management and IoT security platform for service providers. Minim provides operators and their subscribers with cutting-edge fingerprinting, security and network control. The company was inspired by the famous Mirai DDoS against Dyn in 2016 which temporarily disabled parts of the Internet. That attack was the largest DDoS ever and launched from IoT devices.”

He also owns an independent bookstore with his wife.

Minim

After this presentation we finally get to the fun. Minim is an AI-driven Wi-Fi management security platform. It is a software that monitors (security is a part of observability) the home network - it keeps and tracks data like number of devices, type of devices, how much data is a device uploading/downloading, normal hours of connection… The AI then tells you when something looks weird.

Minim has 3 legs, the software running in the cloud with an API, the router software (this one can integrate with the ISP software if the ISP wants to) and the mobile app (to monitor and control the local network).

Currently, their clients are Tier 3 ISPs, small ISPs that have maybe 50,000 or less clients each. The say the are already working on big enterprise deals with bigger ISPs that take a lot of time, but nothing will happen anytime soon.

Centralized cloud observability helps them with more and more devices, another good thing is that there is no need for the router to have Minim software pre-installed for Minim to protect the local network, it just needs the ISP.

Pricing works like this, Minim charges whatever price to the ISP for every local network and then the ISP decides whether to pass it through, include it as a part of higher or premium plan or just offer it as an extra without cost.

I said whatever because we don’t know anything about the financials or metrics of Minim. We do know that the valuation of Minim for the merger was $30M and that it was deemed a third party fair market valuation. All I know comes from the third quarter presentation and conference call (Zoom’s that is) when the Chairman talked about both companies a bit. There is a couple nuggets on the presentation:

First, we can infer the ARPU:

That is $30 a year or $2.5 per month.

The remote worker offering is a move up to the enterprise SMB market that surely is vast more profitable, if this catches some momentum it is worth today’s prices.

Also, I don’t quite know how far the industry affiliations go, but those are nice partners to have.

That may look like 80% gross margins, but it is really more of a goal than an actual number from what I understand after talking with the management.

Signals

I’ll finish with some facts that we know and how they might signal something (or not). Signals are important, they are worth a thousand pictures and I’d rather invest based off a promising signal than a good guidance.

Gray Chynoweth is the CEO of Minim and now of the merged company, it shows that they see value coming from the Minim part (software) of the merger.

Mr. Chynoweth, Mr. Hitchcock and several other members of Dyn are in Minim’s ranks. There is a track record of success here. Also, they are not here for the money, these guys must see something.

Minim realized they need a proof of concept/hero product, Minim is supposed to work fantastically with the Motorolla/Zoom routers, making them the spearhead of their go-to market strategy. It makes sense, and I think they can leverage the hardware channels to expand Minim and viceversa.

David Aronoff, General Partner at Flybridge Capital Partners, Board Member of Draper Laboratories and BetterCloud is an investor and board member of Minim.

Valuation

They biggest constraint I see is capital, so we should expect a raise in the not distant future. I have a small position as it is not very cheap on what we know about Zoom’s base business. Minim is a call, a huge call, surely one to keep track off.