Transmedics, a secular med-tech winner?

Transmedics, a secular med-tech winner?

Finally at a reasonable price!

History of the company

Transmedics was founded in 1998 by its current President and CEO, Dr. Waleed Hassanein. After years of development of the Organ Care System (OCS), in 2019 it floated on the Nasdaq via IPO.

At the time of the IPO the company had pre market approval (PMA) of both Lung and Heart OCS, with the PMA of the OCS Liver to be submitted. By the third quarter of 2021 all three had received PMA and in 2022 the three were approved for organs after either circulatory and brain death donations.

In 2021 growth started to inflect (18% YoY) and in 2022 revenue exploded (200% YoY). They could have probably started their growth journey a bit earlier if it were not for Covid-19 and how it impacted hospitals and delayed the adoption of new instruments and procedures.

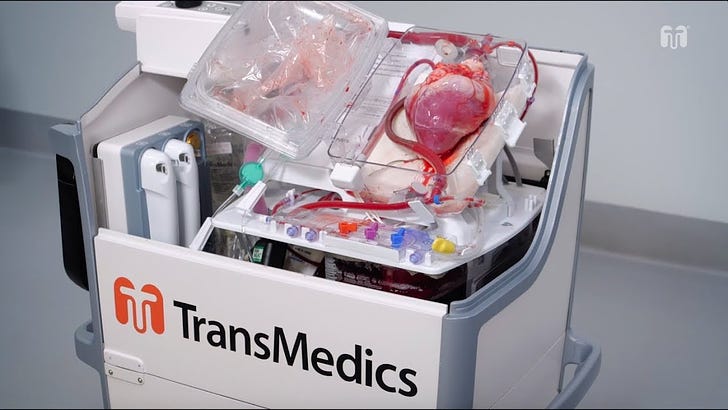

The OCS

I recommend watching the video because it is just an amazing machine

The standard preservation technique (previous to Transmedics’ OCS) was hypothermic conservation of the organs while a suitable recipient could be found. That translates to a fancy version of a box with ice.

The OCS replicates the conditions of the body, while perfusing oxygenated blood, which creates a much more friendly environment for the organ to stay in good conditions until the eventual transplant.

One seemingly logical conclusion is that transplants of organs that have been preserved using the OCS should have better outcomes for the recipient, as the organ should be in better conditions. Also, the OCS broadens the potential pool of recipients that could benefit from the organ.

For the former, there is no strong clinical evidence that suggests substantially better outcomes in transplants that used OCS preserved organs versus just cold storage under 4 hours. From my channel checks, cardiologists tend to prefer (ceteris paribus) an organ that was preserved using the OCS rather than mere cold storage, also, the longer between the death of the donor until the transplant takes place is an important variable when declaring such preferences. If the span of time is just a couple of hours, the benefits of the OCS would not be that impactful, for longer timeframes that preference increases markedly.

As for the broadening of potential beneficiaries of the organs, the OCS allows the transportation of the organs to locations further away that otherwise would be possible. This is a very important selling point in the US, as the potential recipients are spread across the country. The Organ Procurement and Transplantation Network (OPTN) takes distance into account to allocate organs meaning that the OCS unlocks a geographic constrain. In addition, there are some cases when previous to the operation, organs need to be studied further by physicians before assessing the suitability for a transplant, which the OCS also helps by adding time in order to perform more tests.

Before we dwell into how important for the thesis these improvements are, what competitors are doing, the current state of the market and the opportunity for Transmedics, there is a couple of points that are not obvious and increase enormously the potential of the OCS.

First, when it comes to heart transplants (currently the OCS is approved for liver, heart and lungs) traditionally only the hearts of patients that suffered a brain death event – in which the heart and the rest of the organs are still working, but the brain activity stops almost completely – were used in transplants.

In the case of brain death, the organs have been working normally until death occurs and can be kept biologically alive using ventilation or preferably extracorporeal membrane oxygenation (ECMO), in which blood is pumped out of the body to a heart-lung machine that removes carbon dioxide and oxygenates the blood back into the body until the time for the donation comes (this will be important for the second point).

The OCS allows the use of organs for patients that have suffered a circulatory death – when the heart has stopped as well as oxygenation– traditionally, the heart was generally discarded as it had already stopped and a donor that had suffered a cardiac arrest could not be relied upon to provide a well-functioning heart. If a heart has already stopped beating on the donor, it can stop beating after the transplant. It is deemed a damaged organ. The OCS “revives” these organs, expanding the pool of donors and creating a favorable outcome for transplants of these organs. Thus the OCS is creating its own TAM.

Secondly, donations can be an ethical mess. As retrieval of organs has to be made just after death, we are dealing with borderline situations where we could find a patient that is biologically alive, or one that could be kept biologically alive with certain measures but without brain activity (brain death diagnosis is complicated and definitions differ across countries).

This is an ethical issue as some doctors may not find ethically acceptable to remove organs from a body that is still technically alive, even if the brain functions are nil. In these cases, the OCS would remove any ethical consideration since without support, the to be donor would happen to be in a situation of not only brain but also circulatory death. Allowing the doctor to, just after circulatory death has been diagnosed, remove the organs and put them on the OCS without “losing” the heart of the donor.

In some cases of brain death, the organs of the donor are kept inside the body while assistance measures are provided (ECMO) until a suitable recipient is found and ready to accept the organ. With the OCS, the ethical considerations are removed and the preservation of the organs is guaranteed. In fact, when it comes to hearts, the OCS keeps them not only perfused with warm oxygenated blood but the heart keeps beating inside the bag.

Transplants in the US

Transplants in the US go through Organ Procurement Organizations (OPOs) which are nonprofit organizations responsible for recovering organs from deceased donors for transplantation in the USA. There are 57 OPOs, each mandated by federal law to perform this mission in the donation service area assigned to them.

In this write up I will not touch on lungs transplants as they haven’t shown meaningful penetration by the OCS and I don’t believe they can reach high penetration.

Liver transplants have been growing steadily at around 4% per year. In 2022 there were 8,925 transplants of deceased donors, up from 8,667 in 2021. The attractiveness of the OCS here is centered on improved outcomes versus cold storage. I believe that as the OCS evidence on better outcomes in liver transplants mounts, it will increase the penetration (which right now is above 10%)

Hearts are more exciting. As it has been already explained, the stopping of the heart determines one type of death and therefore blood circulation has to halt to declare the donor deceased (circulatory death).

The gap between suitable donors and actual transplants is much wider than in livers, as this organ is more delicate and suitability for recipients is often compromised.

There were 4,111 heart transplants in the US in 2022 up from 3,818 in 2021, the number has been growing at around 5% for the last few years.

(All data above taken from the OPTN)

Both markets are growing, and most importantly, supply of organs is what determines the number of transplants. For example, in 2022 there were 5,072 additions to the heart transplant waiting list, which at a minimum shows that heart transplants could be around five thousand today if there was enough suitable hearts. There is clearly a gap between donors and demand of organs.

Both markets are expected to expand from here on mere population growth and aging (most of the organ demand comes from people 60 and above) but also, as the OCS increases the supply of hearts available for transplantation, the criteria guidelines to get included into the waiting list will probably change and broaden the eventual recipients.

In 2020 Centers for Medicare & Medicaid Services issued a final rule that updated the donation rates and transplant rates for OPOs that must be met to receive Medicare and Medicaid payments. The goal of this final rule was to capture the full potential of donor organs and to hold poorly performing OPOs to national standards. These new conditions went into effect on the 1st of August 2022 and placed greater pressure on OPOs to ensure that donor organs are maximally utilized for organ donation. The push to minimize organ non-utilization lends itself to technologies such as machine perfusion, which may increase utilization, particularly for marginal organs and circulatory death hearts.

The Transmedics opportunity and valuation

Here I try to figure out the market opportunity for the OCS and how we could value Transmedics off it.

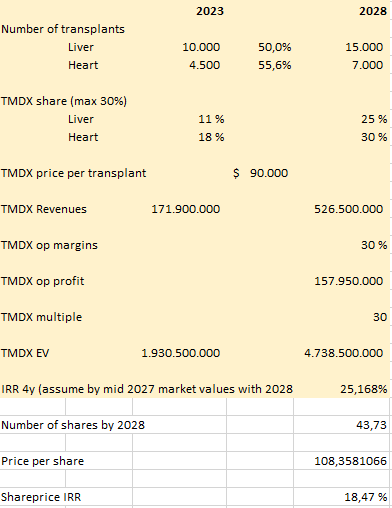

First, I estimate 2028 (5 years from now) figures for heart and liver transplants in the US. (I write off the lung opportunity as I consider it has a low likelihood of success)

By 2028 I assume that the number of heart and liver transplants can grow 8% per year, which is clearly higher that the last 5 years, but I think that the OCS can create an extra supply of organs that can somewhat close the gap between demand and supply for hearts and livers. That results in around 15,000 liver and 7,000 heart transplants in the US.

Then we have to figure out what kind of penetration we would be looking at, that is, how many of those transplants use the OCS to preserve the organ. Transmedics management doesn’t give this kind of information and we have to use ballpark figures. We know they gave the number of 535 organs at some point in April 2023, also, the overall heart penetration is higher than liver. If we annualise these numbers we could get to 1,900 organs runrate in 2023, which would translate in around 13% penetration for liver and heart.

I have them at 11% penetration for liver and 18% for heart in 2023. The heart opportunity is bigger for the reasons exposed, so it is not unreasonable that they could achieve 25% and 30% penetration respectively. Let’s remember that they haven’t grown revenues more because of supply chain constraints and logistic issues (we will address those later).

Those assumptions would give us 5,850 transplants per year, which checks favorably with the stated 10,000 procedures by management.

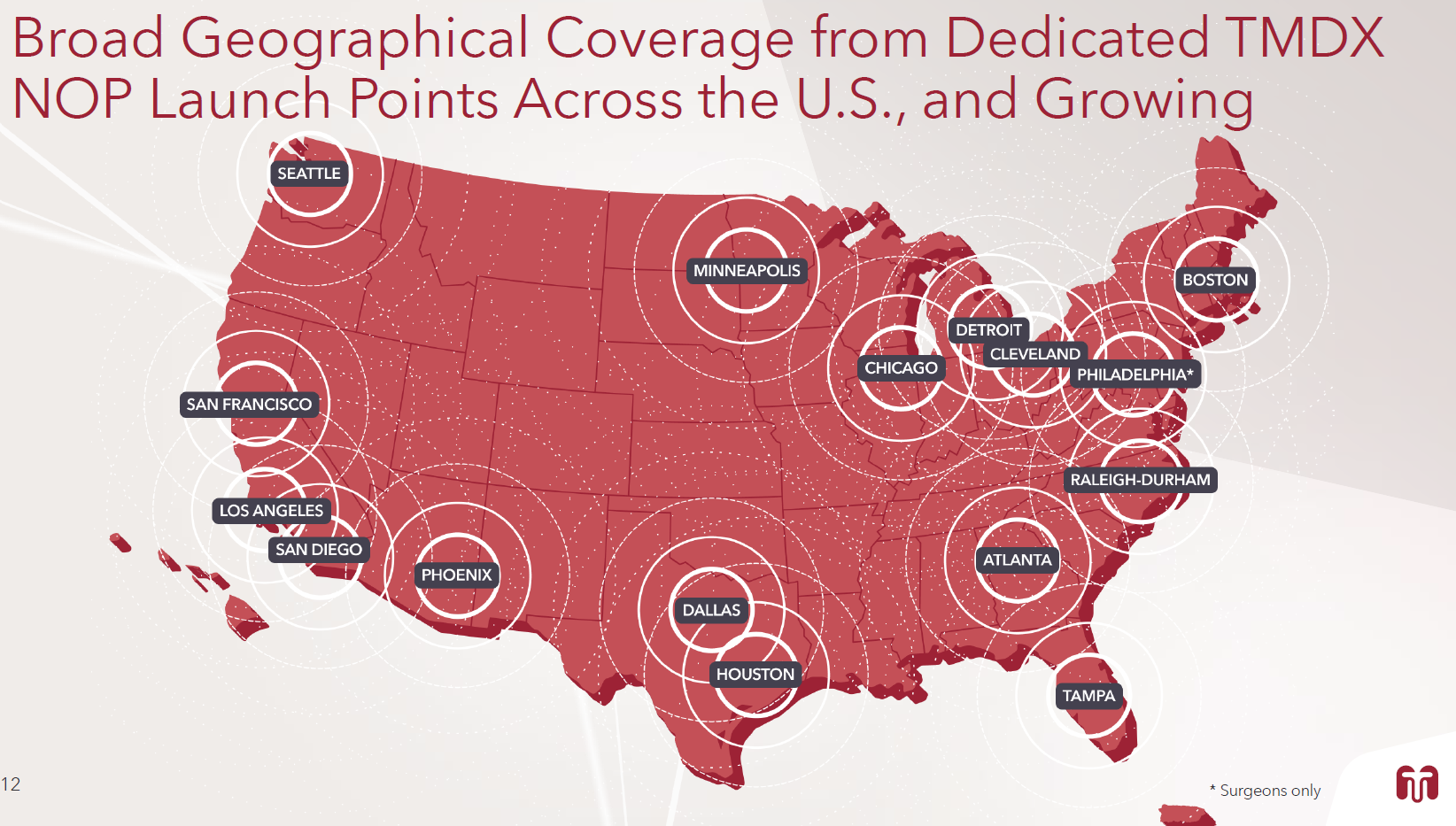

The Transmedics business model is quite simple, the OCS has a disposable part they charge for. The current model consists of a pay per use model. The hospitals don’t pay for the OCS machine, Transmedics figured out that the best go to market strategy was to offer the OCS to hospitals as part of what they call the National OCS Program (NOP), with 16 locations across the US and doctors on the staff it can get to the location of the potential donor and deliver the organ to the destination hospital. This decreases the capex for the hospitals but makes Transmedics not only a med-tech but also a logistics company.

Right now they charge around $90,000 per organ, $60,000 of that is the consumable and the rest would be staffing and logistical costs.

With the numbers provided, we could calculate revenues in 2028 of $526.5 million. (15,000x0.25+7,000x0.3)*90,000

Of course, pricing could (will in my opinion) go up.

Then, it is a matter of margins, Transmedics has shown great operating leverage and although slightly loss making, they won’t be for long. Using other med-tech companies as comparables (Intuitive surgical/Abiomed). Management has guided for long term margins above 30%, I think that 30% EBITDA margins are possible, or at least, the market will value them at those margins if they haven’t reached them by then as long as Transmedics show a clear path to higher profitability.

With 30% margins we would be looking at around $158 million in EBITDA, with a good conversion to FCF (almost 0 capex needed and no debt, leaving just taxes and SBC to detract from the EBITDA)

Now, it is a matter of putting a multiple on that number to see what the total enterprise value would be. I think a x30 EBITDA multiple would be reasonable, in 2028 the business will still have growth ahead, and if they haven’t touched their pricing, that would be a massive lever to pull.

With those numbers we get a TEV of $5 billion.

At $55 per share, Transmedics has a TEV of $1.9 billion with 36.5 million shares fully diluted (33 million shares outstanding + 3.5 million shares of potential dilution + slight net cash that I ignore).

By 2028 we could expect 43.73 million shares (33 million shares + 3.5 million + 2.5 millon of ~1% p.a. SBC/dilution + 4,73 millon from the convertible).

That would mean a price per share of $108 and a 4 year IRR of 18.5% if we assume that by september 2027 the market values Transmedics with the next year numbers.

Although that IRR seems not that great, I am ignoring any price increases and the lung opportunity which have a great upside asymmetry. If they raised prices 20% (from $65k to $78k per consumable) that makes the IRR jump to 22%. If they raised prices 50% we would be looking at a 28% IRR.

Actually, margins will be lower and revenues will be higher as Transmedics internalizes part of the charter expenses, however the profit dollar amount will be around the same as the numbers above. The convertible deal they did in 2023 was in order to get cash to buy planes so they could fix the logistics bottleneck they were going to face/ were already facing.

In general, I deem valuation as a mere approximation to the possibility of outcomes, if it is not cheap using some simple calculations it is not worth trying. Here I have tried to justify what may look like a high revenue multiple (x11 EV/S) and why there is value in the shares.

It is the qualitative analysis that gives me confidence in the future market position of the OCS. US med-tech businesses are really good businesses. The way incentives are set makes for an overuse of devices, a standardization of the use cases, and for entrenched positioning of the devices in the workflow. All of which creates powerful moats and pricing power.

Obviously, the key is to know when a device starts becoming “standard of care” or becomes entrenched in a certain niche. With the OCS we have already seen the emergence of those traits. Medical papers and the general opinion of cardiologists point to that direction.

I like to check against quantitative data too:

Papers that contain the word Transmedics: https://pubmed.ncbi.nlm.nih.gov/?term=transmedics

Citations: transmedics in Publications - Dimensions

Competition and risks

As for competitors, we could name a few:

Cold storage is the main competitor and it will retain a good part of the market as it is the most tested method and it works well enough for organs that have to be outside the donor for less than 4 hours. Cold storage has improved from a box with ice to current devices like the SherpaPak CTS by Paragonix which keeps the heart suspended in a liquid at low temperatures and keeps track of all the variables (temperature, pressure and location), informing in real time.

Other companies with warm perfusion systems; here we can mention Xvivo Perfusion AB, which has a device approved for lungs and another in trial for hearts, the trial for hearts will enroll the first patient in 2023, enrollment for Transmedics’ heart trial was completed by September 2021, that’s a huge head start. XVIVO trades on the Swedish stock exchange and has a market capitalization of $800 million, and their main business is selling products for the traditional hypothermic conservation of organs. Interestingly they found that planes availability was a constraint for their growth too.

We can also mention OrganOx, they have a normothermic machine perfusion device for livers approved by the FDA, and recently raised 25 million pounds. Their device saw some adoption in Europe and in the US it would need more investment to become more widespread. They claim to have performed 2500 liver transplants in the whole world.

In liver, but without FDA approval yet, just mention a couple other devices, LifePort Liver Transporter and VitaSmart Liver Machine Perfusion System. Both are hypothermic instead of normothermic perfusion systems.

Risks to the thesis are mainly related to execution. Transmedics enjoys a first mover advantage in all the organs and competition is very limited. The US medical system favors standardization of devices as more and more data supports safety and clinical evidence of better outcomes, whereas cost is not the number one concern for hospitals. Especially, as transplant costs are eligible for reimbursement and Medicare and private payors assume the bill.

As of the 23rd of September, Transmedics has acquired 8 planes in order to build their logistics network. Although it is the right move and management have shown ability to do what was needed to grow the business this adds another layer of risk. Running a manufacturing and sales operation is one thing, the NOP means being in charge of the logistics and having surgeons and personnel on the payroll. But running a logistical aviation network is a step up.

Personal note: This move and the speed at which the company is deploying capital into the planes is what is probably behind the recent meltdown in the shares

Ideally you want to see rapid adoption from hospitals and more and more surgeons getting used to organs being preserved with the OCS. The possible expansion of the pool of donors and a more widespread use of hearts after circulatory death should happen. Those are the main points to watch for us.

If you got here, thanks for reading!